Deployed trading algorithm based on RSI, MACD and RSP

Algorithmic trading has always been something I wanted to explore due to its potential as a passive income generating tool. The opportunity came when I received an email inviting students to join an algo trading competition. This was hosted by Algogene and the algorithm written was to be tested on IG's Demo Trading Platform.

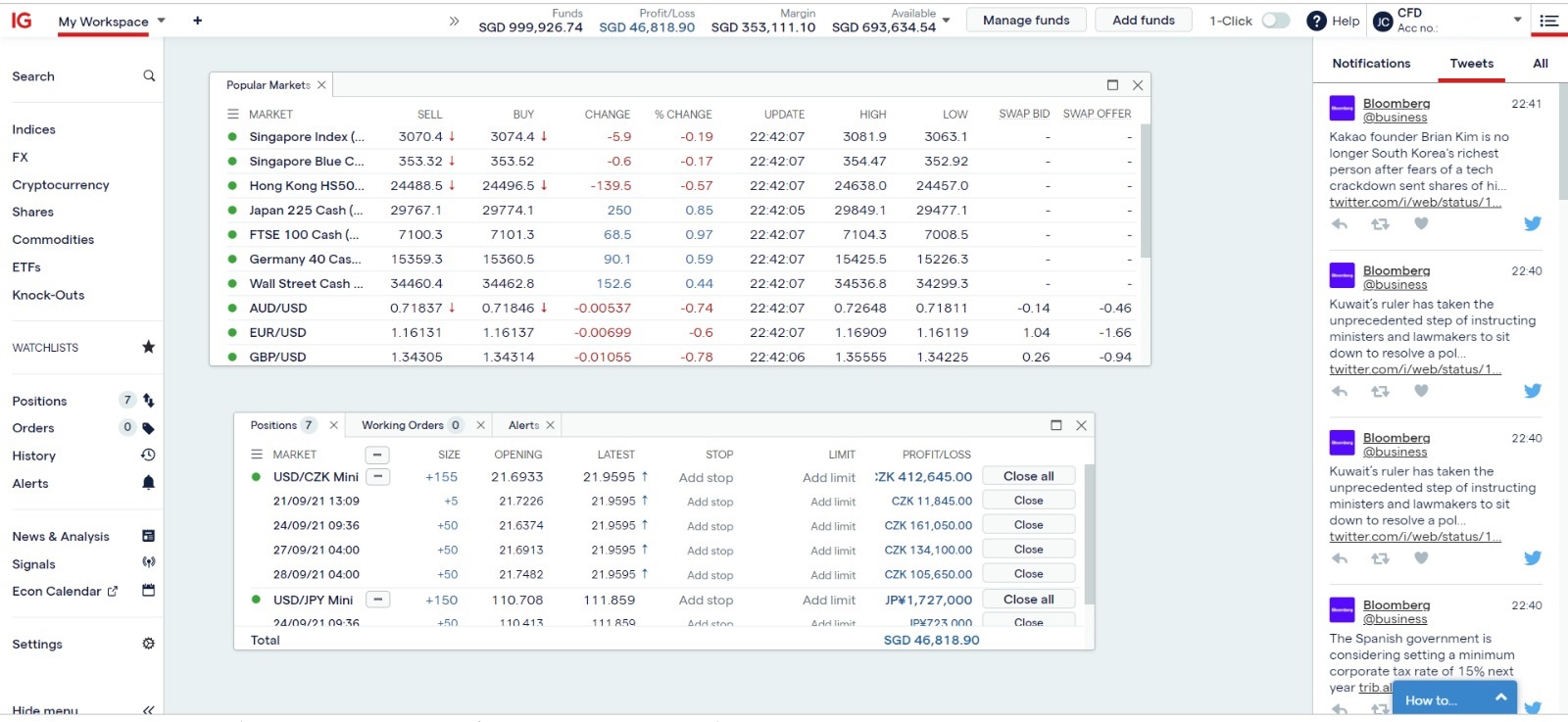

At the point of writing, the strategy and algorithm I developed (with invaluable contributions by Wei Qi) has been running for a week. The performance was compromised due to some technical issues with the order size, but the strategy was still able to be implemented, achieving satisfactory results thus far (although it may have been unfairly biased by the abnormal growth of the US's currency strength during this period).

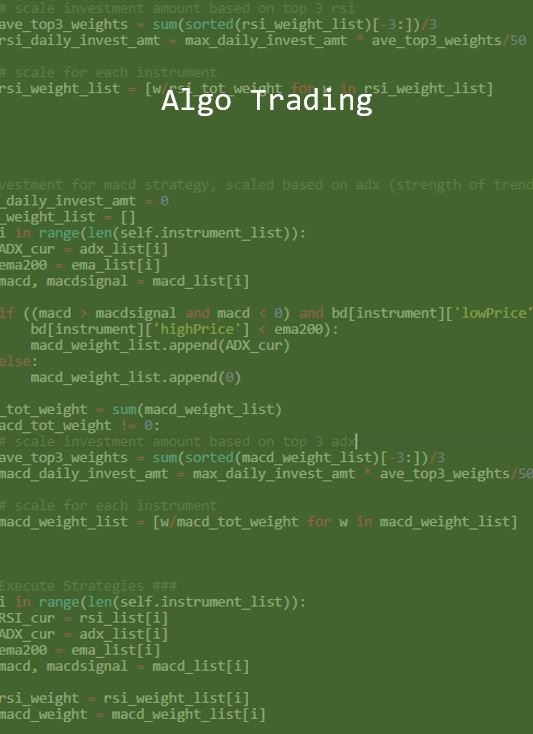

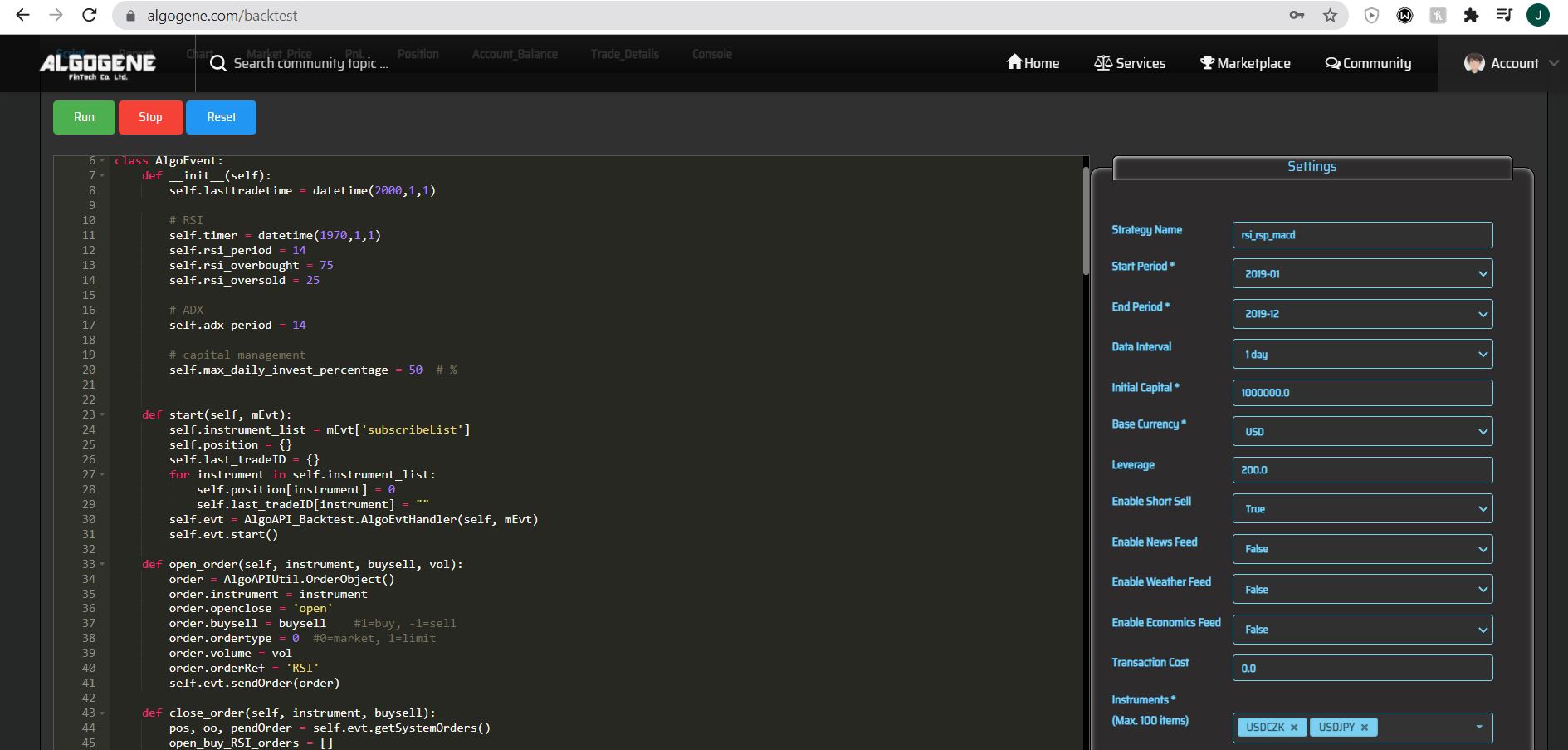

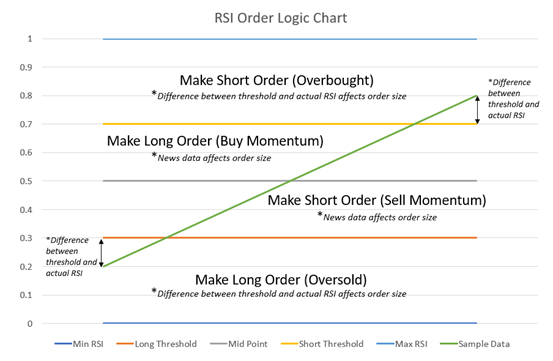

The strategy was relatively simple, I wanted an algorithm that could capture market momentum and find the points where an abnormally high momentum was sustained over a period of time. It turns out the relative strength index (RSI) was the exact indicator I was looking for to translate my idea into a quantity. The remaining parts of the project basically worked around supporting the core RSI strategy, providing alternative conditions to make trades and complementary orders to hedge against the RSI failing. The core ideas are captured below:

This first attempt at algorithm training has been both exciting and educational. At some later point in the future, I intend to deploy an improved algorithm (there is definitely ALOT OF ROOM for improvement) on a live account. You can find the report I wrote explaining the strategy in more detail using the GitHub link in the footer.